Surety bonds can be confusing which is why we’ve compiled a list of surety bond frequently asked questions plus their answers. Don’t see your question here? Ask it in the comment section!

Have questions about bonded titles? Check out our bonded title FAQ.

If you’d prefer to view our interactive FAQ page, you can do so here:

Surety Bonds: Basic Questions

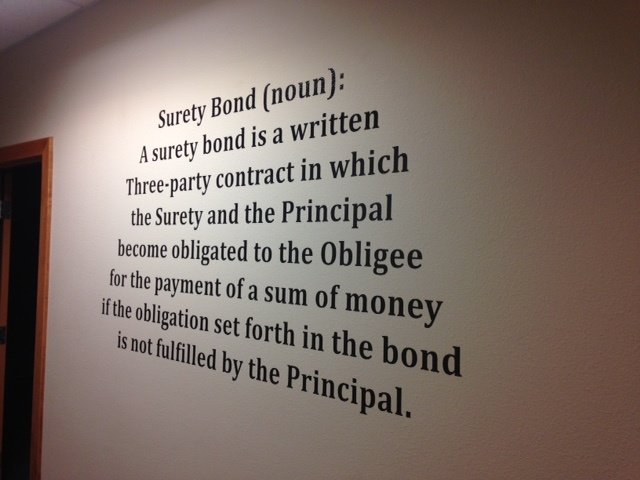

Q: What is a surety bond?

A: A surety bond is a three-party agreement between a principal, an obligee, and a surety.

- Principal: the one who needs the bond

- Obligee: the one who requires the bond and is protected by the bond

- Surety: the one who issues the bond

Essentially, a surety bond promises you will fulfill and perform your duties. If you fail to do so, someone can make a claim against your bond.

Learn more about how surety bonds work.

Q: How do I know I need a surety bond?

A: An obligee (the entity that requires a bond for you to operate legally) will tell you if you need a surety bond. Surety bond requirements vary depending on what you are doing, your occupation, and your location.

Q: Is a fidelity bond the same as a surety bond?

A: No. Fidelity bonds are used to protect companies against financial losses. These are usually optional to obtain, but certain businesses are more at risk than others and are strongly suggested to purchase Fidelity bonds for their company. Companies that are more at risk are:

- Brokerages

- Cash carriers

- Messenger/courier services

- Restaurants/bars

- Boutiques/shops

- In-home service providers (nursing care, pet sitting, security, electronic-installation)

Q: Why can’t I just buy insurance?

A: Surety bonds and insurance are two very different means of protection. Insurance protects the person who buys the insurance. Surety bonds, though, do not protect the person who buys the bond. Instead, they protect the obligee, the person who requires the bond.

Learn more about the differences between surety bond and insurance.

Surety Bonds: Cost Questions

Q: How much does a surety bond cost?

A: The cost of a surety bond depends on many factors. The main factor is the type of bond. A $100,000 surety bond will always cost more than a $1,000 surety bond.

You will not need to pay the full bond amount to get bonded.

You will pay anywhere between 1-15% of the total bond amount.

You only need to pay for your bond one time, NOT monthly. You can learn more here.

The best way to see what you’d pay is to get a free quote below:

Q: So I don’t pay for the full bond amount?

A: No, you only pay a percentage of your total bond amount. Generally, those with strong capital, character, and capacity can get bonded at a 1-3% rate.

Those with bad credit might need to pay anywhere from 4-15% of the total bond amount.

You can use our Bond Cost Calculator to get an estimate on what you would pay for your surety bond.

Q: Can I get a surety bond with bad credit?

A: Yes. We have bad credit options for individuals, so you can get bonded no matter what your situation.

See what you’d pay for a surety bond with bad credit by getting a free quote below:

Get free bond quotes (even with bad credit)

Q: What if I can’t pay for my bond?

A: We have financing options for individuals who need help paying for their bond. Generally, the bond premium needs to be over $1,000 for you to qualify for financing.

Surety Bonds: Application Questions

Q: What is the process to get a surety bond?

A: Here are the steps to get a surety bond:

1. Submit an application

2. An underwriter will evaluate your risk and determine your bond rate

3. View quotes

4. Sign indemnity agreement

5. Pay for bond

After you pay for your bond, the surety company will mail you the completed bond. Some bonds can be downloaded right after you pay for them, but not all bonds.

You can learn more about how to get a surety bond here.

Q: What is an indemnity agreement?

A: An indemnity agreement is a legal document that fully discloses your obligations in the surety bond relationship. It allows the surety bond company the right to recover any losses paid out on behalf of you.

Q: Do indemnity agreements expire?

A: The indemnity agreement is a part of the bond and is active during the entire lifetime of the bond. Indemnity agreements are typically signed and submitted with the bond application. If the bond is never issued, the principal would be required to sign a new indemnity agreement if reapplying for the bond.

Q: Why does my spouse have to sign the indemnity agreement?

A: Sureties often require that a spouse personally guarantees your surety bond. This is because most personal assets are shared with your spouse. This simply ensures that the personal assets used for underwriting are available to the surety bond company should a claim be made on your bond.

Q: How long does it take to get a bond?

A: The length of time from application to issuance will vary depending on the type of bond. Many bonds can be approved instantly online upon completion of an online application. Other bonds can be issued one to two days after receipt of payment and a signed copy of the indemnity agreement.

Certain bonds can be downloaded right after you pay for them, but not all bonds. If your bond cannot be downloaded, it will be mailed to you. We (Surety Solutions) provide free USPS shipping or you can pay for overnight shipping for an additional $20 at checkout.

Browse available bonds and apply online.

Surety Bonds: Claims Questions

Q: What happens if a claim is filed against my bond?

A: Read this post on Surety Bond Claims.

If a claim is made on your bond, the surety bond company will investigate the claim to determine if it is valid or not.

- If the claim is not valid, there will be no financial losses incurred since the dispute was deemed illegitimate.

- If the claim is valid, though, the surety bond company will remind you of your obligations under the indemnity agreement and give you the opportunity to satisfy the claim.

If you fail to respond or satisfy the claim, the surety bond company will arrange a settlement with the obligee, then proceed with collecting the settlement from you.

Q: How can I avoid claims on my bond?

A: Run an ethical business and fulfill your obligations and duties that are laid out in your surety bond contract.

Car dealers can learn more about how to avoid bond claims here.

Mortgage professionals can learn more about how to avoid bond claims here.

Now that you are all educated, ready to get your bond?