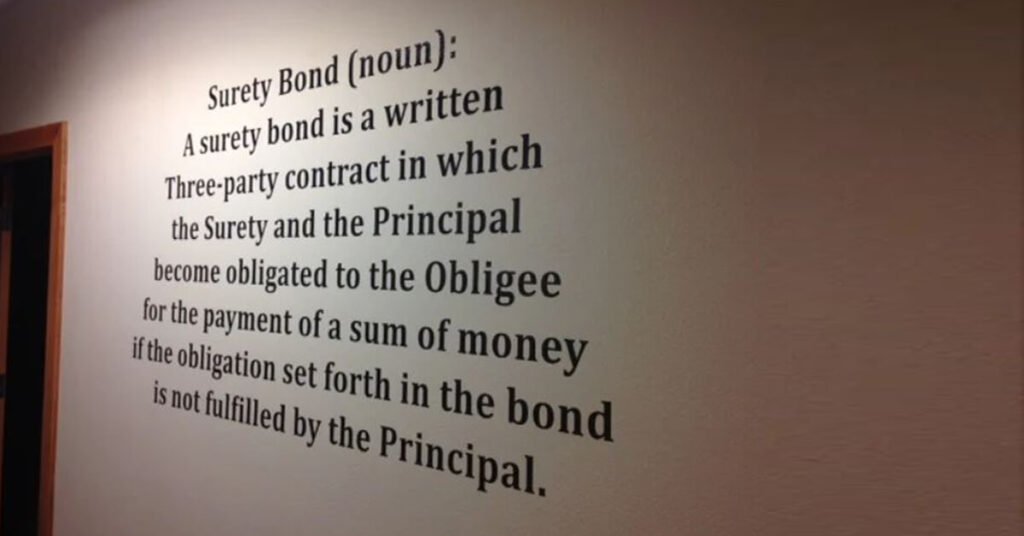

As stated above, you don’t need to have the full funds to purchase a Surety Bond. Even if you do have the available funds in full, you don’t have be concerned about having a large amount of your funds frozen in an account.

A Surety Bond is generally easier to get when compared to a Letter of Credit. You don’t need to have an established relationship with a surety company, whereas this is necessary for a Letter of Credit. However, you may end up paying more in premium with a Surety Bond, since a Letter of Credit typically doesn’t cost more than 1% of the amount required by the contract.

What happens if a claim is made on a letter of credit?

Hello Laura,

Excellent question! A claim against a Letter of Credit can be made by the Beneficiary. The financial institution that issued the letter of credit will review any documentation submitted by the beneficiary to verify the claim is valid. The funds associated with the Letter of Credit will be dispersed among the claimants.

Comments are closed.